Bitcoin Myths · #2 of 20

Bitcoin Is Volatile. Every Emerging Asset Was.

Bitcoin’s price swings are real. So are the Venezuelan bolívar’s, the Turkish lira’s, and the Nigerian naira’s. Volatility is what early adoption looks like in an asset with fixed supply and no central issuer. The volatility has been declining with each market cycle. And in economies where local currencies are collapsing, it is already beside the point.

The criticism is easy to make from a stable currency. Bitcoin swings 20% in a month, and the headline writes itself. Too risky, too unpredictable, and too volatile to be useful.

The argument has a comparison problem. “Too volatile” compared to what? To the dollar and the S&P 500, or to the naira, the lira, and the bolívar? The answer changes depending on where you are standing.

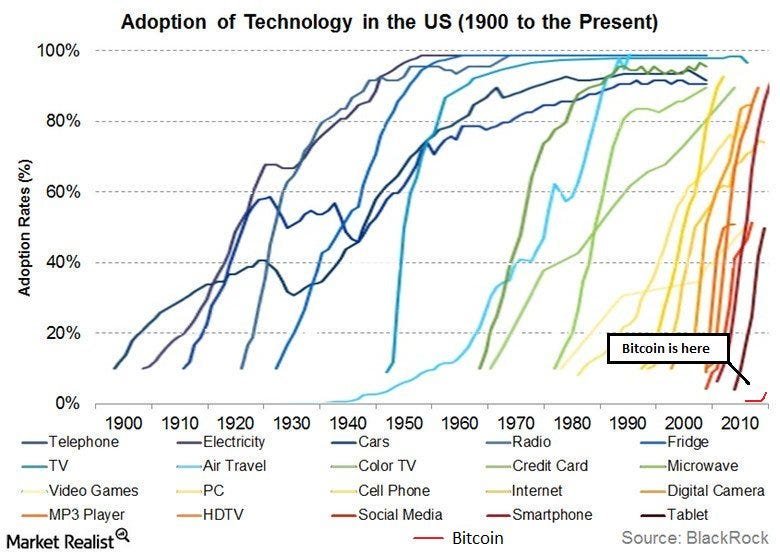

And even setting that aside, the criticism treats Bitcoin as a finished product. It is not. It is a 15-year-old monetary network still in the middle of global adoption.

Bitcoin is not just an emerging asset. It is attempting something rarer, monetizationThe slow process of something becoming money, as more people hold it for its own sake and it takes on a monetary premium.. Every good that has acquired a monetary premium went through violent repricing first, while markets worked out what that premium was worth. Gold after Bretton WoodsThe 1944 agreement that pegged world currencies to a gold-backed US dollar. It collapsed in 1971, and gold’s price swung wildly for years afterward.. The dollar before it became the global reserve currency. Equities before institutional frameworks gave them liquidity and legitimacy. High volatility is what price discoveryA market feeling out what something is worth through buying and selling, before the price settles into a steady range. looks like on an open market with no central issuer and a fixed supply. Bitcoin’s monetary rules do not change with inflation targets or election cycles. The volatility is in demand, not in the asset itself. Leverage and derivatives amplify it further, pushing swings past what fundamentals alone would produce. But the underlying dynamic is the same. Demand for new money is uncertain until it is not.

That base is growing. Bitcoin’s annualized volatility ran around 140% in its early market cycles. It has since settled in the 45 to 55% range, still higher than established equity markets, but roughly half what it was. Methodologies vary, but the direction is consistent across approaches. Each cycle has shown lower peak-to-trough swings than the last as institutional capital entered, liquidity deepened, and long-term holders increased as a share of the market. Source: Glassnode volatility data

Bitcoin has been the best-performing major asset class of the past decade, returning more than stocks, bonds, and gold. Source: Fidelity Digital Assets

Bitcoin Volatility Against Hyperinflationary Currencies

In Turkey, the lira lost 44% of its value in 2021. Not in a crash. Not in a black swan event. In an ordinary year, as a consequence of monetary policy. In Nigeria, the naira routinely loses 30 to 40% of purchasing power annually. In Venezuela, Lebanon, and Zimbabwe, the numbers are worse.

From those countries, Bitcoin’s volatility can look preferable to guaranteed currency debasement.

The “too volatile” argument assumes a stable alternative. For most of the world’s population, that alternative does not exist. Bitcoin competing with the dollar is one conversation. Bitcoin competing with the naira or the bolívar is a different one entirely.

| Country | What Bitcoin competes with |

|---|---|

| Venezuela | The bolívarVenezuela’s national currency. lost almost all its value over a decade of hyperinflation. Bitcoin became a practical tool for preserving wealth and moving money across borders when banks failed and cash became worthless. |

| Nigeria | The nairaNigeria’s national currency. loses 30 to 40% of purchasing power annually. Nigeria has one of the highest Bitcoin adoption rates in the world. More than 30% of adults have used it, primarily for peer-to-peer transactions and bypassing capital controls. |

| Turkey | When the lira fell 44% in 2021, Bitcoin adoption spiked. For Turkish savers, Bitcoin’s short-term swings were less damaging than holding their own currency through the year. |

| Argentina | Currency controls make dollar access difficult and the official exchange rate fictitious. Bitcoin bypasses both the black market and the capital control system simultaneously. |

| Lebanon | A banking collapse froze deposits and destroyed savings. Bitcoin, which no bank can freeze, became a way to hold and move value outside the system entirely. |

| Zimbabwe | Long synonymous with hyperinflation, Zimbabwe has seen Bitcoin adoption as a store of value where the local currency offers none. Saving in bitcoin means purchasing power goes up as local prices go up. |

Source: Livingston, Adam. The Bitcoin Age, Chapter 3: Challenges and Misconceptions. © 2025.

Bitcoin for Payments and the Lightning Network

Most people holding Bitcoin today are not trying to buy coffee with it. They are holding it because they would rather own a fixed-supply asset than keep cash in a system they distrust. That is the primary use case today, and volatility does not undermine a store-of-value argument. A rising long-term price with short-term swings is still a rising long-term price. Many would rather hold than spend.

For everyday transactions, the Lightning Network handles it, with instant settlement and near-zero fees, running on Bitcoin’s base layer. The infrastructure exists. Adoption of the payment layer follows adoption of the base asset, and that process is still underway.

The comparison the myth skips

The volatility criticism expects Bitcoin to already behave like a mature monetary system. It is not one yet. It is running without a central bank, a board of directors, or a lender of last resort. Every currency transition in history involved an adjustment period where the new system looked unstable relative to the old one.

There is a distinction worth making here. Bitcoin’s price is volatile. Bitcoin’s monetary policy is not. The supply cap and the issuance schedule never change, and no committee votes on them. Contrast that with fiat currencies. Prices appear stable day to day, but the monetary rules governing them shift constantly with political cycles, inflation targets, and emergency interventions. Bitcoin has volatile price discovery and stable rules. Fiat has stable optics and unstable governance. Depending on which kind of certainty you are optimizing for, those are very different propositions.

The real question is not whether Bitcoin is volatile. It is which kind of certainty matters more to you. Stable prices in a system where the monetary rules keep changing, or stable rules in a system where the price keeps moving? That is a question worth sitting with. “Is it volatile?” is not.

Go Deeper

The case for hard money, and why sound monetary rules matter more than price stability. The chapter on time preference is the clearest frame for why volatility is not how you evaluate Bitcoin as money.

A history of money and the structural fragility of fiat, directly on the volatility-versus-debasement tradeoff this article explores. Alden is strongest on why apparent fiat stability is not the same as monetary soundness.

The Bitcoin Age

Country-by-country documentation of Bitcoin adoption in high-inflation and capital-restricted economies, including the Venezuela, Nigeria, Turkey, Argentina, Lebanon, and Zimbabwe cases in this article. The most grounded account of what Bitcoin competing with collapsing currencies looks like on the ground.

Want the shorter version? The Did You Know post covers this one in brief, and the infographic version lays out the argument in one shareable one-pager.

Prefer to watch?

This myth is also a short video. It walks through the same evidence, the six cycles of volatility data, the comparison most people skip, and why the price moves, in a few minutes.

Common Questions About Bitcoin Volatility

Is Bitcoin too volatile to be money?

Bitcoin is still in the monetization phase, the same phase gold and the dollar went through before liquidity deepened. Its volatility has declined substantially with each market cycle and continues to trend lower. In economies where local currencies lose 30 to 40% of purchasing power annually, Bitcoin’s swings are already the more stable option.

Why is Bitcoin so volatile?

It comes from two things. First, a fixed supply with no central bank to smooth demand shocks. Second, market-driven amplification from leverage and derivatives. Both decrease as the holder base matures and liquidity deepens.

Has Bitcoin volatility decreased over time?

Yes. Annualized volatility ran around 140% in Bitcoin’s early cycles. According to Glassnode data, it has since declined to roughly 45 to 55%, with the trend continuing lower each cycle.

Is Bitcoin more volatile than gold?

Yes, in the short term. Gold has centuries of monetary history and deep institutional liquidity. Bitcoin is 15 years old. The better comparison is Bitcoin now versus gold during its own monetization phase, when gold’s price was also highly sensitive to demand shifts.

Why do people in high-inflation countries use Bitcoin despite its volatility?

Because the alternative is worse. Where local currencies lose 30 to 40% annually, Bitcoin’s price swings are often less damaging than holding local currency. The volatility argument assumes a stable alternative. In much of the world, that alternative does not exist.

Twenty myths. Twenty clean answers.

Explore all 20 myths →More from the Bitcoin Myths Series

Everything on this site is for educational purposes only. It is not financial, investment, tax, or legal advice. Bitcoin carries real risk. Prices move. Do your own research, think for yourself, and speak with a qualified professional before acting on anything you read here.